In the modern fiscal landscape, the historical logic of “bigger is better” in banking has been replaced by the logic of precision. According to the McKinsey Global Banking Annual Review, the competitive gap is no longer defined by branch density, but by an institution’s ability to embed responsible AI and high-touch digital engagement directly into daily workflows.

The most visible battleground for this precision? The messaging channel.

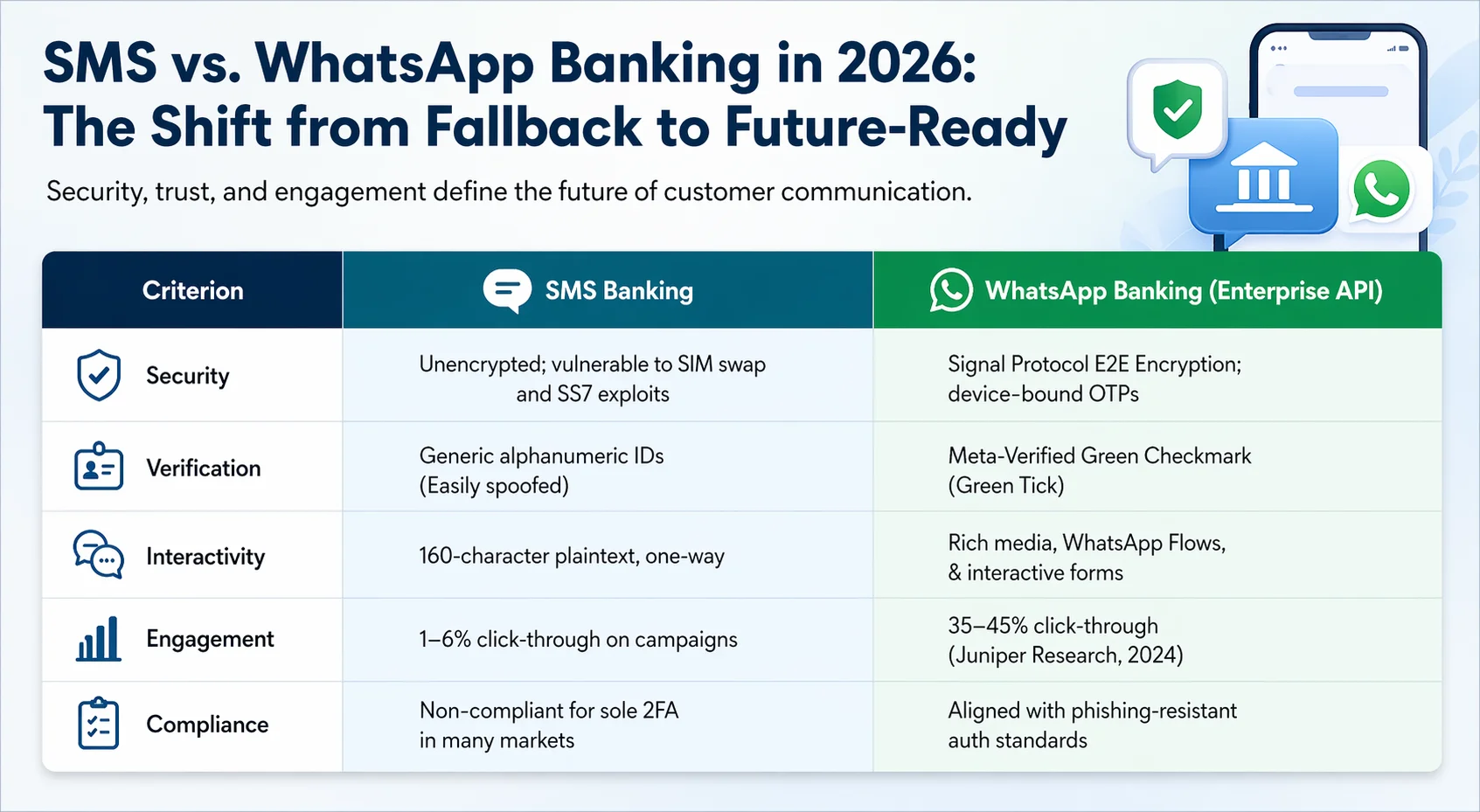

For two decades, SMS was the undisputed king of bank-to-customer communication. But as of 2026, regulatory mandates and shifting user behaviors have reclassified SMS from a “primary channel” to a “compliance fallback.”

The Foundations: SMS and WhatsApp in 2026

What is SMS Banking?

In its simplest form, SMS Banking is the use of Short Message Service (SMS) to deliver banking notifications, one-time passwords (OTPs), and balance alerts. It operates over standard cellular networks, requiring no internet access or smartphones.

Why SMS Banking Still Matter

In its simplest form, SMS Banking is the use of Short Message Service (SMS) to deliver banking notificatDespite the rise of richer channels, SMS remains a strategic necessity for three reasons:ions, one-time passwords (OTPs), and balance alerts. It operates over standard cellular networks, requiring no internet access or smartphones.

- Universal Reach: It reaches 100% of mobile users, including those on legacy feature phones.

- Regulatory Backstop: In markets like India, the RBI still mandates SMS alerts for high-value transactions to ensure delivery regardless of a user's data status.

- The "Last Resort" Failsafe: When data networks are congested, SMS serves as the critical emergency notification layer for fraud alerts.

What is WhatsApp Banking (Enterprise API)?

WhatsApp Banking is the use of the official WhatsApp Business API to deliver regulated financial services through conversational messaging. Unlike personal WhatsApp, the Enterprise API allows banks to automate onboarding, support, and sales with end-to-end encryption and full integration into the bank’s core systems.

The 2026 Comparison: Security, Scale, and the "Trust" Factor

What is SMS Banking?The Strategic Necessity of Orchestration

Modern institutions aren’t just looking for “another app.” They are looking for Unified Omnichannel Banking Platforms that handle complexity. As noted in Deloitte’s 2026 Banking Outlook, retail banks must go beyond a “product lens” to create experiences that are data-driven and consistent across every channel.

Regulatory Deadlines: The Catalyst for Change

The shift from SMS to encrypted messaging is now a legal requirement in several high-growth jurisdictions:

- UAE — CBUAE Mandate: As of March 31, 2026, the Central Bank of the UAE has mandated the elimination of SMS and email OTPs for authentication. Liability for fraud linked to legacy channels now rests on the institution.

- India — RBI 2FA Expansion: The RBI’s revised authentication framework requires that for digital payments, one factor must be cryptographically tied to the device—a standard WhatsApp natively supports.

Segment Strategies: From Retail to Corporate Efficiency

1. Retail: The End of "App Fatigue"

Retail success in 2026 is measured by friction reduction. By deploying AI-powered Onboarding Solutions, banks are compressing account opening from days to minutes.

- Impact: Institutions using i-exceed’s Appzillon platform report a 40–60% reduction in call center costs by migrating routine support to WhatsApp-based AI agents.

2. Corporate & SME: Control and Treasury Visibility

SME owners manage their businesses via WhatsApp. Banking delivered through the same channel feels native rather than burdensome.

- Multi-Stakeholder Approvals: A Director approves a high-value wire transfer via an encrypted WhatsApp message, logged and audit-ready.

- Treasury Visibility: Real-time balance positions and FX alerts pushed directly to the treasury team.

- Case in Point: Global leaders like Citi have demonstrated the power of this by rolling out Digital Corporate Onboarding across 90+ countries.

How to Implement WhatsApp Banking : The 90-Day Roadmap

For a Tier-1 or Tier-2 bank, implementation is no longer a multi-year project. By using an API-first orchestration layer, banks can follow this streamlined path:

- Phase 1 — Selection & Compliance (Weeks 1-3): Choose a Business Solution Provider (BSP) and align on data residency requirements

- Phase 2 — Core Integration (Weeks 4-8): Use a low-code platform like Appzillon to act as a bridge, connecting your existing data to the WhatsApp API without replacing your core.

- Phase 3 — UAT & AI Training (Weeks 9-11): Deploy your AI Knowledge Base to handle routine FAQs and set up human-agent escalation protocols.

- Phase 4 — Go-Live (Week 12): Launch with a high-impact use case, such as SME onboarding, to see immediate ROI.

Conclusion

The strategic question for bank leaders in 2026 is no longer about the “if”—it is about the “how.” SMS banking remains your compliance backstop, but WhatsApp banking is where your growth, security, and customer loyalty will be won.

The technology is ready. The regulators have spoken. The only remaining variable is the decision to act.

To know more about how i-exceed can help with your digital banking initiatives, get in touch with us at marketing@i-exceed.com .

Frequently Asked Questions

The key differences are security, interactivity, and regulatory trajectory. SMS is unencrypted, limited to 160-character text, and vulnerable to SIM swap attacks. WhatsApp is end-to-end encrypted, supports rich media and interactive forms, and is structurally resistant to SMS-based fraud. For authentication, regulators in the UAE have already eliminated SMS OTPs entirely. For engagement, WhatsApp generates 6–10x higher click-through rates. For compliance in 2026, WhatsApp banking is aligned with the regulatory direction of travel across the UAE, India, and Europe.

Yes, when deployed through the official WhatsApp Business API. All messages use Signal Protocol end-to-end encryption — widely regarded as the gold standard for messaging security. Business identity is Meta-verified, preventing impersonation. Enterprise deployments include full conversation audit trails, role-based access controls, and data residency options. WhatsApp banking is significantly more secure than SMS for authentication, because it cannot be compromised by SIM swap attacks or SS7 interception.

WhatsApp banking is in production at banks across more than 100 countries. In India, banks including Kotak Mahindra Bank, HDFC Bank, ICICI Bank, and SBI offer WhatsApp banking services. Globally, institutions including Citi have deployed WhatsApp for corporate onboarding across 90+ countries. According to Meta’s 2024 figures, over 60% of banks worldwide are using the WhatsApp Business API for at least one banking interaction.

Modern digital banking platforms use API-first, microservices architecture to add WhatsApp as a channel without requiring changes to core banking infrastructure. The platform handles WhatsApp Business API integration, authentication, session management, compliance logging, and AI conversation management. Banks connect their existing core banking data to the platform via APIs. i-exceed’s Appzillon platform is an example of this approach — banks have reported deploying new WhatsApp journeys 70% faster than traditional development timelines.

Requirements vary by market. Core requirements include: customer opt-in consent before business-initiated messages; use of pre-approved Meta message templates; complete conversation logging with timestamps; data residency compliance per local regulations (GDPR in Europe, DPDP Act in India, CBUAE data regulations in UAE); and integration with the bank’s existing KYC, fraud monitoring, and AML systems. Deployment must be through a Meta-accredited Business Solution Provider.