For a business owner running a marketplace in Jakarta, a construction firm in Dubai, or a law firm in Mumbai, knowing your total balance is easy—knowing who paid it is the nightmare. Traditional banking forces an impossible choice:

1. Administrative Chaos: Open 100 physical accounts for 100 projects – each with its own KYC, fees, and “account sprawl.”

2. Reconciliation Hell: Use one massive account for everything and spend 40+ hours a month matching bank transfers to invoices like a forensic accountant.

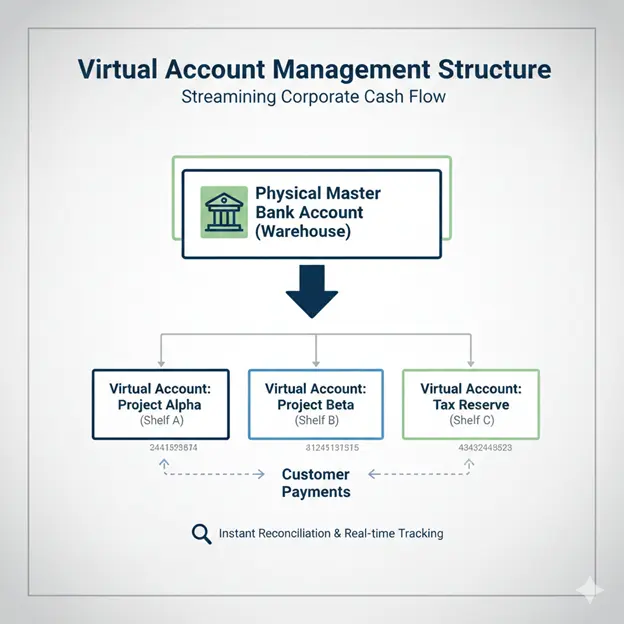

Virtual Accounts (VAs) solve this by decoupling the Payment Identifier from the Legal Ledger. A virtual account is a unique, “shadow” account number that routes funds into a master physical account.

How Do Virtual Accounts Work?

Think of the physical account as a warehouse; virtual accounts are the shelving units.

A virtual account is a sub‑ledger linked to one physical account. It has a unique identifier (e.g., VA number or virtual IBAN) for routing and granular reporting; funds settle in the master account, not the VA. They allow for the partitioning of funds—for payroll, tax, or specific client projects—without the overhead of opening 100 physical accounts.

The Banking CXO’s Dilemma: We Have the Engine, But No Dashboard

The Execution Gap is not in the Core; it is in the Engagement Layer. Corporate treasurers rank real‑time cash visibility and API connectivity among their top modernization needs- a sentiment echoed by McKinsey’s research on the imperative for banks to move beyond transaction-led models to engagement-led platforms.

Why Legacy Portals are Costing You Deposits:

- Zero Self-Service: Corporates want to create, name, and close accounts in 60 seconds, not via PDF forms.

- Data Fragmentation: The VAs exist in the core, but the portal shows a flat, unsearchable list of 5,000 numbers with no hierarchy

- API Silence: If a corporate’s ERP (SAP, Oracle, NetSuite) cannot programmatically "ask" your bank for a new VA, they will move to a fintech competitor who can.

For the Business Owner: The Three Pillars of Virtual ROI

1. Zero-Touch Reconciliation

The old way: “Payment received from ABC PVT LTD.” Your team spends 20 minutes cross-referencing which of the five “ABC” clients it was.

The VA Way: Assign “Customer A” their own permanent VA number. When money hits that number, your system knows it is Customer A. Period. Marketplace platforms in India have reduced reconciliation time from 8 days to 4 hours using this exact logic.

Leading banks report that virtual accounts streamline receivable matching and reduce reliance on multiple physical accounts, with self‑service structures available via portal and API.

2. Operational Agility (The "60-Second Account")

Opening a physical account is a 3-week journey of KYC and branch visits. A virtual account is a 60-second self-service task on a modern banking portal. For a construction firm with 15 active projects, being able to create “Project-Specific Pockets” instantly is the difference between profit and administrative bloat.

3. Liquidity Visibility

The Strategic Blueprint for 2026: Orchestrating the VAM Experience

Layer 1: The Backend Engine (The "Core")

Layer 2: The Engagement Layer (The "Experience")

This is where the battle for the corporate client is won. A modern engagement layer- like the one provided by Appzillon– sits on top of your Core and delivers:

- Self-Service Hierarchy Management: Drag-and-drop interfaces that allow treasurers to organize accounts into "folders" (e.g., APAC Ops > Singapore > Project Alpha).

- Embedded Analytics: Moving beyond balance reporting to Treasury Intelligence. "Your UAE entity has $2M in excess liquidity; suggest an inter-company sweep to cover Saudi expansion."

- API-First Delivery: Exposing RESTful APIs so your corporate clients can integrate their ERPs directly into your VAM engine.

- ERP/TMS Connectors: Pre‑built API endpoints for balance & transactions, VA creation/maintenance, and payment initiation, enabling real‑time feeds into SAP/Oracle/NetSuite TMS/ERP.

Regional Mandates: APAC and the Middle East

APAC: The Marketplace Scale

The “Gig Economy” in India and Southeast Asia is creating a massive need for FBO (For-Benefit-Of) structures. The e-Conomy SEA report by Google and Bain & Co. shows that digital payments in the region are scaling at a 20% CAGR, driven largely by these multi-vendor marketplaces.

A delivery platform with 50,000 vendors needs 50,000 virtual accounts. If your portal crashes when displaying more than 500 rows, you cannot win this segment. You need a portal designed for scale and bulk operations.

Middle East: Conglomerates and Shariah Compliance

- Multi-Entity Reporting: Aggregating balances by legal entity and by business unit.

- Shariah-Compliant Partitioning: The ability to segregate Halal funds within a larger master account hierarchy without co-mingling.

The Roadmap to VAM Leadership (6-9 Months)

1. Audit the “UI/UX Friction” (Month 1): How many clicks does it take for a corporate to see their total liquidity? If it’s more than two, you’re losing.

2. Decouple the Front-End (Month 2-3): Don’t wait for a Core Banking upgrade. Implement a digital engagement layer that can talk to your existing VAM backend via APIs.

3. Launch a Pilot (Month 5): Choose 10 high-volume SMEs. Give them a self-service dashboard. Watch their “Time-to-Task” drop.

4. Monetize Through Value (Month 9+): Once the CX is frictionless, you can move from “Free Accounts” to “Premium Treasury Management” subscription models.

Accelerated Path: By utilizing a low-code digital engagement layer, banks can bypass the traditional 12-month development cycle and launch a functional VAM MVP in as little as 90 to 120 days.

Conclusion: The New Competitive Moat

In 2026, the moat is no longer your balance sheet; it is your interface. Virtual accounts are the most powerful tool in the corporate banking arsenal, but they are useless if trapped behind a legacy UI. The banks that win—and the businesses that thrive—will be those that embrace Self-Service VAM as the core of their digital identity.

Is your corporate banking portal a strategic asset or a competitive liability?

FAQs

A virtual account is a sub‑ledger linked to a single physical account that uses unique identifiers (such as virtual IBANs) to route and track payments, while all funds settle in the master account. This provides granular visibility without opening multiple physical accounts.

Virtual accounts let businesses assign unique account numbers to customers, departments, or invoices, ensuring automatic identification the moment funds arrive—drastically reducing manual reconciliation and errors. Major banks report significantly faster and more accurate reconciliation using VA‑based structures.

Corporate treasurers now expect real‑time cash visibility and API‑enabled account creation/maintenance, but most legacy portals lack these capabilities. Industry research shows both banks and corporates highlight real‑time visibility and API connectivity as top modernization priorities.

Yes. Banks increasingly expose API endpoints for VA creation, maintenance, balance inquiry, and transactions, enabling direct ERP/TMS integration. This removes batch delays, improves forecasting accuracy, and enables real‑time treasury operations.

Absolutely. APAC’s rapid growth in real‑time payments and open‑finance ecosystems has made virtual accounts essential for handling large‑volume, multi‑party collections with instant reconciliation—especially for marketplaces and gig‑economy platforms.

Virtual accounts help Islamic banks maintain segregation of funds, auditability, and Shariah‑compliant oversight, aligning with emerging regulatory frameworks in markets like the UAE and Bahrain. This ensures clean fund flows and transparent governance in digital treasury operations.