The financial services landscape is currently undergoing its most significant transformation since the invention of the credit card. We have moved beyond the era of “Digital Banking” (simply putting a web interface on top of a bank) into the era of API Banking.

But here is the reality: for many institutions, API banking still feels like a ‘compliance tax.’ In this guide, we shift that perspective – showing how APIs move beyond regulatory checkboxes to become your most profitable product line in 2026.”

Quick Takeaways for 2026 that you can take from this blog:

- Security: FAPI is the new mandatory standard for high-value transfers.

- Growth: Embedded Finance is the #1 driver of new deposit volume.

- Bottom Line: APIs are products, not just tools. Treat them with a dedicated P&L.

Part I: The Architecture of Modern API Banking & Banking APIs

Building a banking API is fundamentally different from building a generic web API. The stakes involve real-time financial data, regulatory oversight, and the requirement for “five-nines” (99.999%) availability.

Why Your CTO and CFO Finally Agree

API banking isn’t just about ‘better code.’ It’s about agility. In a legacy environment, launching a new loan product takes 18 months. With a mature API architecture, you can test a new partner integration in 18 days. Here is the technical foundation that makes that speed possible:

1. The Core Infrastructure Layer

To support an API ecosystem, banks must move away from monolithic legacy cores. Modern API banking requires a Microservices Architecture to support Open Banking APIs and embedded finance APIs, ensuring scalability and compliance. By breaking down banking functions—such as “Check Balance,” “Transfer Funds,” or “Identity Verification”—into independent services, banks can update specific features without risking the stability of the entire system.

- Service Mesh: Using tools like Istio or Linkerd to manage internal communication. In 2026, a Service Mesh is critical for implementing a Zero Trust architecture, ensuring that even internal "east-west" traffic is encrypted via mTLS.

- Event-Driven Architecture (EDA): Financial transactions are events. Utilizing Kafka or RabbitMQ allows the bank to process transactions asynchronously, providing a snappier experience for the end-user while maintaining a robust audit trail on the backend.

2. The API Gateway: Preventing Downtime While Scaling Traffic

The API Gateway is the most critical component of your external infrastructure. It acts as a single entry point for all third-party developers.

- Rate Limiting & Throttling: Protects the core banking system from being overwhelmed by spikes in traffic or DDoS attacks.

- Protocol Transformation: Modern gateways can take legacy SOAP requests from older internal systems and transform them into clean, developer-friendly RESTful JSON for external partners.

Securing the Vault: Beyond Simple Authentication

In banking, a single security flaw is a catastrophic event. As of 2025-26, standard API keys are no longer sufficient. You must implement a Zero Trust security model.

Advanced Security Protocols

- mTLS (Mutual TLS): Ensures that both the client and the server verify each other's certificates, creating a secure, encrypted tunnel.

- OAuth 2.0 & OpenID Connect: The gold standard for authorization. Instead of sharing credentials, third parties use short-lived "Access Tokens."

- FAPI (Financial-grade API): A specialized security profile for high-value transactions that requires even stricter signing and encryption than standard OAuth.

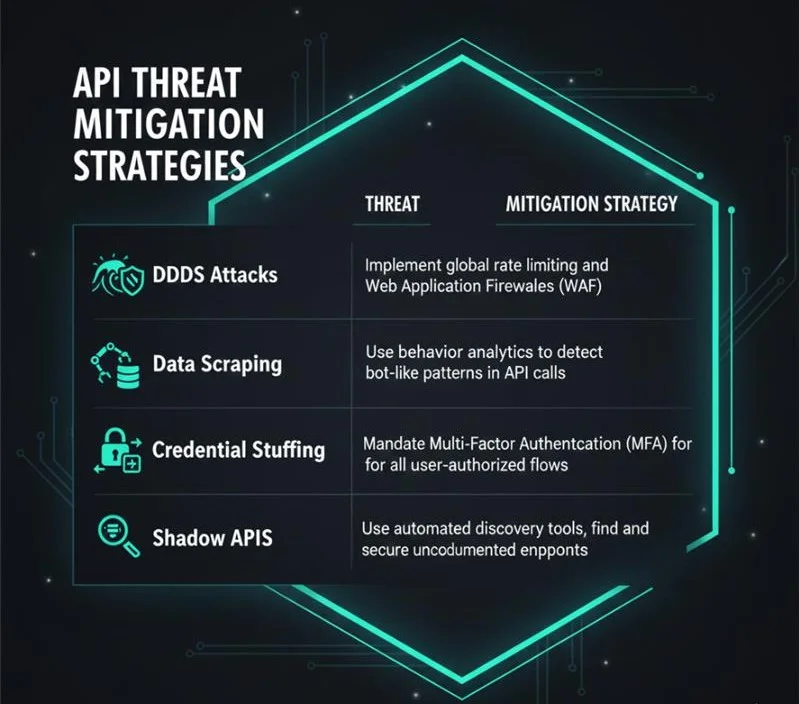

Threat Mitigation Strategies

| Threat | Mitigation Strategy |

|---|---|

| DDoS Attacks | Implement global rate limiting and Web Application Firewalls (WAF). |

| Data Scraping | Use behavior analytics to detect bot-like patterns in API calls. |

| Credential Stuffing | Mandate Multi-Factor Authentication (MFA) for all user-authorized flows. |

| Shadow APIs | Use automated discovery tools to find and secure undocumented endpoints. |

- Pro Tip: Always use Opaque Tokens for external communication to hide sensitive internal data structures from potential attackers.

3. Developer Experience (DX) as a Competitive Advantage

In the API economy, the developer is the new customer. If your API is difficult to use, developers will migrate to a competitor.

- Documentation: Use the OpenAPI Specification (OAS) to create interactive documentation.

- The Sandbox Environment: You must provide a "mock" environment where developers can test their code using synthetic data. A bank that requires a 30-day manual approval process just to access a sandbox has already lost the market. To stay ahead, leading institutions are turning to platforms like i-exceed’s Appzillon, which leverages a low-code, micro-app architecture to reduce the end-to-end onboarding and development time by more than 50%.

- Pro Tip: Always use Opaque Tokens for external communication to hide sensitive internal data structures from potential attackers.

Part II: Securing the Digital Vault

Security in API banking and API security standards like FAPI and OAuth 2.0 are critical for PSD3 compliance and global Open Banking mandates. With the rise of AI-driven cyberattacks in 2026, traditional username/password authentication is obsolete.

1. The Zero Trust Framework

Banks must adopt a Zero Trust approach: “Never trust, always verify.” Every single API call, whether it comes from a trusted partner or an internal app, must be authenticated and authorized.

2. Financial-Grade API (FAPI) Standards

While standard OAuth 2.0 is sufficient for social logins, the 2026 standard for high-value transactions is Financial-grade API (FAPI). The OpenID Foundation’s FAPI provides a higher security profile. FAPI mandates the use of JWS (JSON Web Signatures) and mTLS, providing the level of non-repudiation required for modern regulatory compliance under PSD3.

- mTLS (Mutual Transport Layer Security): Unlike standard HTTPS where only the client verifies the server, mTLS requires the client to present a certificate as well.

- The Sandbox Environment: Ensures that the payload of the API request has not been tampered with during transit.

3. Consent Management and PSD3 Compliance

With the evolution from PSD2 to PSD3 in Europe and similar “Open Banking” mandates in the US and Brazil, consumer consent is paramount.

- Fine-Grained Scopes: A user shouldn't have to give an app access to their entire transaction history just to verify their account balance. APIs must allow for "limited-time" and "limited-purpose" access.

- Dynamic Linking: For payments, the authentication must be linked to a specific amount and a specific payee, preventing "man-in-the-middle" attackers from altering the transaction details.

Part III: Monetization Strategies – Turning Banking APIs into Products

Many banks view APIs as a “compliance tax” forced upon them by regulators. However, the most successful banks treat APIs as a product line with its own P&L, leveraging API monetization models such as Banking-as-a-Service APIs and tiered pricing strategies.

1. The "Banking-as-a-Service" (BaaS) Model

This is the most lucrative monetization path. The bank provides its regulated infrastructure to non-banks.

- Example: A ride-sharing app wants to offer "Instant Pay" to its drivers via a branded debit card. Instead of becoming a bank, the app uses your APIs to issue cards, manage ledgers, and process payments.

- Revenue: The bank earns through "per-account" monthly fees and interchange revenue from card swipes.

2. Tiered Subscription Models

Borrowing from the SaaS playbook, banks can offer different levels of API access:

- Free/Essential Tier: Access to public data (ATM locations, branch hours, currency exchange rates).

- Professional Tier: Access to account balances and transaction history for a flat monthly fee.

- Enterprise Tier: High-throughput access to real-time payment initiation and bulk data webhooks.

3. Unit-Based Pricing

Charging for the outcome rather than just the connection.

- KYC-as-a-Service: If a fintech uses your API to verify a customer’s identity (using your existing robust compliance checks), you charge $1.00 per successful verification.

- Credit Scoring APIs: Providing a "Probability of Default" score based on transaction data can be sold to lenders as a premium API call.

4. Revenue Sharing (The Ecosystem Model)

In some cases, the bank might pay the developer. If a third-party app uses your API to bring in a new mortgage lead or a high-net-worth deposit, the bank shares a portion of the customer’s lifetime value with the partner.

Part IV: Implementing API Governance

To manage 1,500+ endpoints across multiple regions, a bank needs a rigorous API Governance framework. Without it, you end up with “API Sprawl”—a disorganized mess of redundant and insecure endpoints.

1. Design Standards

Every API in the bank should “look and feel” the same. This means consistent error codes (e.g., using standard HTTP 404 for Not Found), consistent date formats (ISO 8601), and consistent naming conventions (camelCase vs snake_case).

2. Versioning Strategy

Banking APIs cannot simply change overnight. You must support older versions while transitioning users to new ones.

- Header-based versioning: Accept: application/vnd.bank.v2+json

- Sunsetting Policies: Give partners at least 12–18 months' notice before retiring an API version.

3. Observability and Monitoring

You cannot manage what you cannot measure.

- Latencies: Are your payment APIs responding in under 200ms?

- Error Rates: Are you seeing a spike in 401 Unauthorized errors? This could indicate a credential stuffing attack.

- Business Metrics: Which partners are generating the most transaction volume?

Part V: The Future – Embedded and Conversational

As we look toward 2030, the “interface” of banking will disappear. This is the era of Embedded Finance.

1. Non-Financial Platforms

Banking will happen where the customer already is. If a small business is using accounting software like QuickBooks, they shouldn’t have to log into a separate bank portal to pay a vendor. The “Bank API” lives inside the accounting software.

2. AI-to-API Interaction

We are entering a world where “AI Agents” will act on behalf of humans. A user might tell their AI, “Find the best savings rate and move $5,000 there.” Your bank’s APIs must be discoverable and “readable” by AI agents, not just human developers.

3. Cross-Border Interoperability

With initiatives like the BIS Nexus project, banking APIs are becoming standardized across borders. Building your APIs to be compatible with global standards ensures you can participate in the worldwide instant-payment network.

4. The Voice-First Revolution- Agentic Voice Banking

In 2026, the interface of banking is shifting from “eyes and thumbs” to “voice and ears.”

Voice banking has evolved beyond basic IVR menus into autonomous AI voice agents.

- API-Driven Conversations: Modern voice assistants use Speech-to-Intent APIs to bypass complex app navigation. A user can simply say, "Move $200 to my travel fund and tell me if I have enough left for rent," and the API orchestrates the balance check and transfer in one flow.

- Voice Biometrics: As a security measure, banks are now using Voice ID APIs that analyze pitch, speed, and accent patterns as a form of multi-factor authentication, making voice banking as secure as a fingerprint.

Conclusion: Building the Bank of Tomorrow

The journey to API maturity is not a sprint; it is a fundamental re-engineering of the banking business model. By focusing on a robust microservices architecture, financial-grade security, and creative monetization models, traditional banks can not only survive the fintech revolution but lead it.

The banks that win in 2026 and beyond will be those that realize their most valuable asset isn’t the money in their vaults—it’s the data in their APIs.

Conclusion: Your Next Steps

API banking is no longer an “IT project”—it is the core strategy for any bank that wishes to remain relevant in a decentralized, digital-first world. Success requires balancing the openness needed for innovation with the rigor required for security.

FAQs

API Banking refers to the use of Application Programming Interfaces (APIs) by banks to enable secure, real-time data exchange and functionality between banking systems and third-party applications. It powers open banking, embedded finance, and Banking-as-a-Service models.

Banking APIs are software interfaces that allow external applications to access banking services such as account information, payments, KYC, and transaction processing. They help banks integrate with fintechs, partners, and non-financial platforms seamlessly.

Banking APIs are critical for innovation and growth. They enable faster product launches, embedded finance experiences, and new revenue streams through Banking-as-a-Service. APIs also support compliance with global open banking regulations like PSD3.

Banking APIs act as secure gateways between a bank’s core systems and external applications. They use protocols like REST or GraphQL and security standards such as OAuth 2.0, mTLS, and FAPI to ensure safe, authorized data exchange.

Modern API Banking requires Financial-grade API (FAPI) standards, OAuth 2.0, OpenID Connect, and mutual TLS (mTLS). These ensure strong encryption, consent management, and compliance with regulations like PSD3 and Open Banking mandates.

Banks monetize APIs through Banking-as-a-Service (BaaS), tiered subscription models, unit-based pricing (e.g., KYC-as-a-Service), and revenue-sharing partnerships. APIs are treated as products with dedicated pricing and performance metrics.

The future of API Banking includes AI-driven interactions, voice-first banking, cross-border interoperability, and embedded finance. APIs will become the backbone of banking ecosystems, enabling seamless integration with everyday platforms.